PNV 2025: Rising Revenue Masks a Continued Market Contraction

By Tim Carl

Support Napa Valley Features – Become a Paid Subscriber Today

If you’re reading this, you care about independent, locally owned, ad-free journalism — reporting that puts our region’s stories first, not corporate interests or clickbait.

As local newsrooms are increasingly bought by billionaires, scaled back or absorbed into media conglomerates, communities lose original reporting and are left with more syndicated content. Your support keeps quality regional journalism alive.

Join a community that values in-depth, independent reporting. Become a paid subscriber today — and if you already are, thank you. Help us grow by liking, commenting and sharing our work.

PNV 2025: Rising Revenue Masks a Continued Market Contraction

By Tim Carl

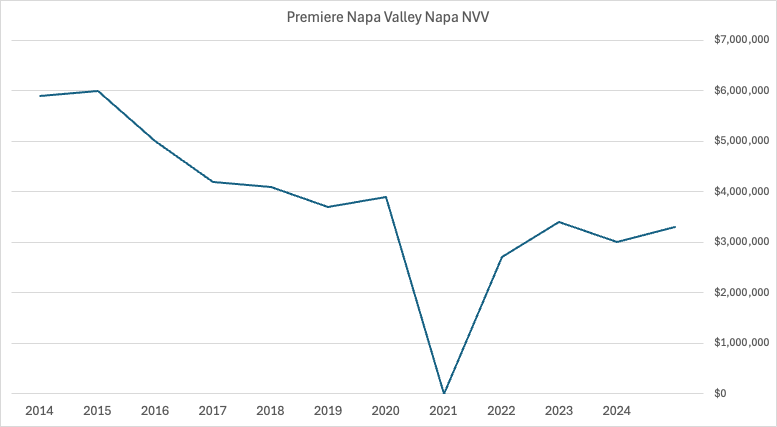

NAPA VALLEY, Calif. — The 2025 Premiere Napa Valley auction, held last weekend and organized by Napa Valley Vintners, raised $3.3 million — a 10% increase over 2024’s $3 million. While this event had increased participation by wineries and visible enthusiasm by attendees for the highly anticipated 2023 vintage, it fell significantly short of the auction’s peak in 2015, when it raised $6 million with an average per-lot price of $26,667. In contrast, the 2025 average per-lot price dropped to $17,010 — a 36.2% decline from the 2015 peak and a 5.3% decrease from a year earlier.

The number of lots has increased in recent years, rising from 137 in 2023 to 167 in 2024 and then to 194 in 2025. However, these figures remain below the 225 lots offered in 2015.

Unlike public charity auctions, PNV is a trade-only event where wineries offer exclusive barrel lots to wine retailers, restaurants and distributors. These buyers use the auction as a barometer to gauge demand and assess the quality of vintages like the highly anticipated 2023 wines featured this year. Yet despite the enthusiasm for this vintage and increased winery participation, the declining per-lot averages signal that the market remains under strain.

Even focusing on the more recent years, from 2023 to 2025 the average per-lot price has fallen, signaling a market still contracting rather than stabilizing. Buyers are stretching their budgets rather than bidding aggressively. This trend suggests ongoing pressure on pricing, aligning with broader concerns in the 2024 Preliminary Grape Crush Report and recent direct-to-consumer shipment data.

Vintage Quality and Market Uncertainty

The 2025 auction featured wines predominantly from the 2023 vintage, which many winemakers and critics have described as age-worthy, structured and balanced due to its long, steady growing season. The reds, many tasted as barrel samples, showed firm tannins and higher-than-normal acidity, suggesting excellent aging potential, while the whites were widely praised for their clarity and freshness.

“Overall, we were impressed with the 2023 reds,” said Gary Fisch, a long-time attendee and advocate of Napa Valley wines. “It was difficult to find a wine you didn't like. This was one of the most universally superior vintages at PNV, from our experience. This made it challenging to pick lots we wanted to go for due to the high quality of the vintage.”

While such optimism translated into bidding, conversations throughout the weekend reflected caution.

One buyer, who requested anonymity, said that while there was significant enthusiasm for purchasing the vintage, much of it seemed driven by a desire to support friends in Napa Valley rather than genuine retail demand: “From a consumer standpoint, demand for wines at these price points has dropped significantly and there were a lot more empty chairs at the auction compared to past years.”

High-End Buyers vs. Mid-Tier Struggles

Pricing pressure and caution from buyers aligns with broader challenges in the wine market, including oversupply, slowing demand and shifting consumer preferences, as also highlighted in the 2024 Preliminary Grape Crush Report, with the bulk of cabernet sauvignon grapes (in the $8,001-$14,000 per-ton range) seeing a drop in tonnage purchased, reflecting wineries’ scaling back.

While there remains a belief that high-end buyers are somehow insulated from the current wine market slowdown, even they seemed to be pulling back at this year’s event.

The top-performing lot at the 2025 Premiere Napa Valley auction was 60 bottles of Simon Family Estate 2024 Cabernet Sauvignon (anticipated to be released in 2027), which sold for $60,000 to Gregor Greber, a Zurich-based buyer and frequent attendee at the auction. This marked a significant decline in the top bid compared to recent years. In 2022 Greber placed the highest bid of $100,000 for 60 bottles of BRAND 2021 Cabernet Sauvignon, meaning the top bid has fallen by 40% over the past three years.

Other notable lots this year included 60 bottles of The Mascot 2024 Cabernet Sauvignon, which fetched $55,000, as well as 120 bottles of Quintessa 2023 Cabernet Sauvignon and 60 bottles of Hourglass 2023 Cabernet Sauvignon, both selling for $50,000 each. Additionally, JennaMarise Wines/Robert Foley Vineyards secured $49,000 for 240 bottles of their 2023 Cabernet Sauvignon.

More Winery Engagement, More Spending on Events

While bidding trends and average lot prices suggest caution, maybe not surprisingly, overall engagement from wineries at PNV 2025 was notably higher. Wineries invested heavily in side events, private tastings and buyer-focused experiences throughout the multiday series of gatherings leading up to the auction. From exclusive vineyard lunches to intimate tastings at high-profile estates, the focus was clear — building stronger long-term relationships with buyers.

“Overall, it was a great week of PNV events showcasing the '23 vintage, Fisch said. “From a buyer's perspective, it was challenging to get to open houses because so many events overlapped.”

Though difficult to quantify, the apparent increased spending on hospitality signals that vintners recognize the urgency of securing buyer loyalty in a shifting market. One vintner who asked to remain anonymous noted, “It’s no longer enough to just make great wine from the Napa Valley. You have to create an experience and relationships that buyers remember. We are pulling out all the stops.”

What Does This Mean?

Critics might contend that relying on average auction lot prices as a metric for assessing market interest or pricing pressure has its limitations, as it does not account for changes in the mix of wines offered or shifts in costs over time. To ensure accuracy and provide further context, we reached out to NVV to share our findings and seek clarification or confirmation of the data. They initially questioned our 5.3% decline year-over-year number, so we sent them the calculation, which you can see in the note below.* Additionally, we requested a direct comment on our analysis, which are outlined in the Editor’s Note below. Nonetheless, these figures offer a valuable lens into broader market trends and underscore the challenges facing Napa Valley's wine industry.

For consumers, this could signal a turning point. While price reductions haven’t been widespread, downward pressure is building. If current trends persist, the coming year may bring more opportunities for buyers, particularly in segments that have historically resisted discounting.

Napa Valley Vintners relies on this auction as both a fundraiser for promotional efforts and a barometer for industry sentiment. This year the message was clear: While the wine-buyer support for Napa Valley wines remains robust, the market remains cautious about the near future.

In a press release, Linda Reiff, president and CEO of NVV, emphasized the importance of industry collaboration in sustaining momentum: “This year’s auction results show the deep commitment of our trade partners and the exceptional quality of the 2023 vintage,” Reiff said. “We’re thrilled to see this level of engagement and grateful for the continued collaboration.”

Yet beneath such optimism many questions remain. Will wine demand continue to decline, or is the wine industry, including Napa’s, facing a long-term market correction? How much more will vintners need to invest in improved sales strategies as traditional distribution tightens?

Editor’s Note: Just prior to publication, NVV reached out to clarify that publicly reported auction figures are rounded, and beginning in 2024, total revenue figures now include the 8% auction fee. Additionally, the composition of auction lots has varied, such as the inclusion of Vintage Perspective Tasting wines in 2023, which were not directly comparable to standard Premiere Napa Valley lots, making direct comparisons challenging.

While these adjustments provide further context, they do not fundamentally alter the overall trend of declining per-lot revenue and broader market pressures. Our calculations are based on widely published data, but adjusting for the 8% cost structure change beginning in 2024 would shift the 2024 YoY decline from -27.6% to approximately -21.3%, with no impact on the 2025 YoY percentage decline (-5.3%).

As in any industry, inflation and rising operational costs influence pricing dynamics, including at auctions. NVV also suggested that 2014 and 2015 auction totals may have been anomalies. They have been invited to share more detailed information, including cost and revenue data, for further analysis, and we will report back with any changes.

Looking Ahead

The decline in the average per-lot price from its peak underscores a contracting market. Even in the more recent period from 2023 to 2025, per-lot averages have continued to fall despite a growing number of lots. While high-end buyers remain active, the highest bids have steadily declined in recent years, signaling broader pricing pressures across the market.

At the same time, recent data show that direct-to-consumer wine shipments fell 10% in 2024, and January shipments declined another 15%, and recent grape sales data suggest Napa Valley wineries are pulling back, too. This all suggests that even Napa Valley’s producers — long insulated by brand prestige — must adjust to a shifting marketplace where annual price increases at retail are no longer guaranteed.

The biggest takeaway? Napa Valley’s wine industry is actively attempting to turn the tide of slowing wine sales but is also not immune to larger market forces. While the industry presents a strong front, the underlying numbers reveal a more nuanced and challenging reality — one that requires adaptation, continued strategic repositioning and a recalibration of expectations.

For consumers, this could signal a turning point. While price reductions haven’t been widespread, downward pressure is building. If current trends persist, the coming year may bring more opportunities for buyers, particularly in segments that have historically resisted discounting.

—

*Note: For those wanting to see our calculation of the decline in per-lot revenue, for example the 5.3% decline in per-lot revenue from $17,964 in 2024 to $17,010 in 2025, the calculation follows a standard percentage change formula: (New Value – Old Value) ÷ Old Value × 100. Plugging in the numbers, (17,010 – 17,964) ÷ 17,964 × 100 = -5.31%, confirming that per-lot revenue decreased by 5.3%. The data for lot numbers comes from articles and press releases (2015, 2023, 2024, 2025), while the total dollar amounts come from both our internal database and press releases or articles (2015, 2023, 2024, 2025).

Tim Carl is a Napa Valley-based photojournalist.

Today’s Polls

Explore These Related Articles:

Browse All Napa Valley Features Stories

I manage a wine shop in Ohio. Despite the "glut" of California wine, I have yet to have a single winery lower their prices. In fact, they are still raising them. DAOU cab just went from 24.99 to 28.99 up 16%. Sounds like they are waiting for this year's short harvest to fix things.

Tim Carl’s excellent financial analyses of Napa County’s major issues is one of the primary reasons I am a paid subscriber.